On March 15, 2024, the National Association of Realtors® (NAR) announced a $418 million settlement with a nationwide class of plaintiffs in an antitrust lawsuit. The lawsuit centered around claims that Realtors® conspired to artificially inflate commission rates by not being transparent about how buyer’s agents are compensated.

So, what’s changing about how buyer’s agents are compensated?

Today, when a seller’s agent lists a home on a REALTOR®-owned Multiple Listing Service (MLS), they are able to include an offer of compensation to the buyer’s agent as part of the listing. Moving forward, this compensation cannot be advertised on the MLS.

The practice of putting the buyer’s agent commission percentage on the MLS has led many to believe that number is fixed. And many agents have not done a good job explaining that commissions are negotiable.

If the court approves NAR’s settlement, agents will no longer be able to advertise any buyer’s agent’s compensation when they list a home on a REALTOR®-owned MLS. This will encourage agents to have more in-depth conversations with their clients around compensation, promoting greater transparency across the industry.

Lastly, buyers will now be required to sign buyer’s agency agreements to ensure they fully understand the buyer-broker relationship, obligations between broker and client and how their buyer’s agent is compensated.

All in all, it’s too soon to tell exactly how the proposed rule change will impact the housing market. What we do know is that there are too few homes and too much demand — even with current mortgage rates — for home sellers to worry about competing on price, generally speaking.

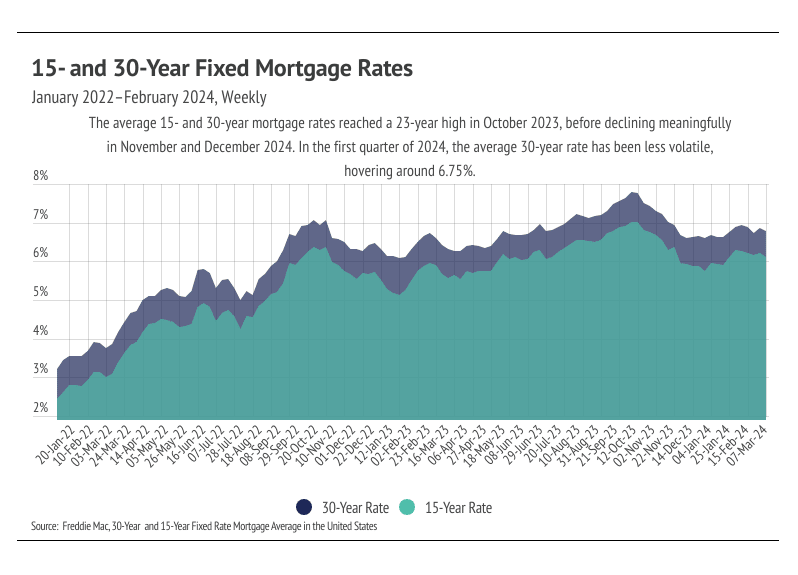

Speaking of mortgage rates, the Federal Reserve held rates steady at the March meeting, which was in line with expectations. With the information from Fed Chair Powell, we are now expecting rate reductions after the June or July Fed meetings. The Fed’s dual mandate aims for stable prices (inflation ~2%) and low unemployment. Employment has shown its persistent strength, and inflation is coming down, but the Fed wants more good data before lowering rates because they want to avoid raising rates once they’ve started lowering them.

Overall, the market is starting to heat up, which is what we expect and want to see this time of year. Mortgage rates have been elevated for long enough now that buyers and sellers are less hesitant to enter the market. And rate cuts will come in the second half of the year, allowing for refinancing in the near future. As a result, we are expecting far more transactions than last year and a healthier market.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data

The Local Lowdown

-

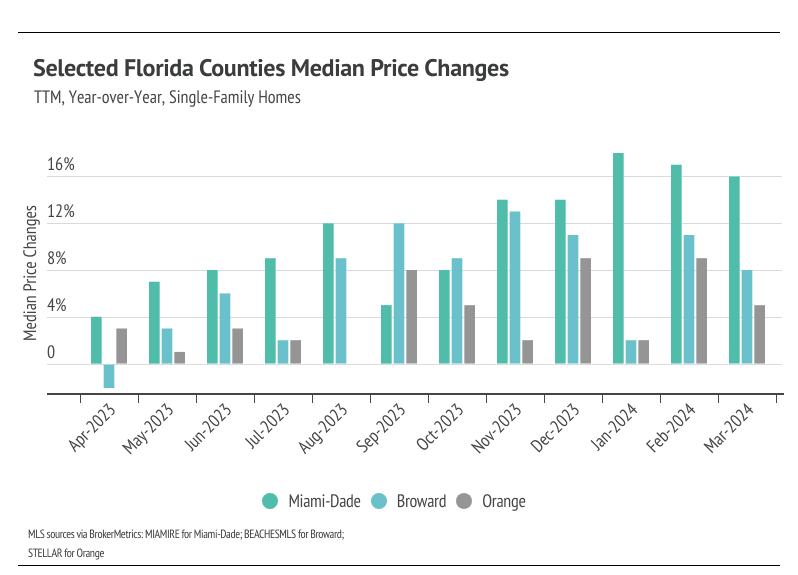

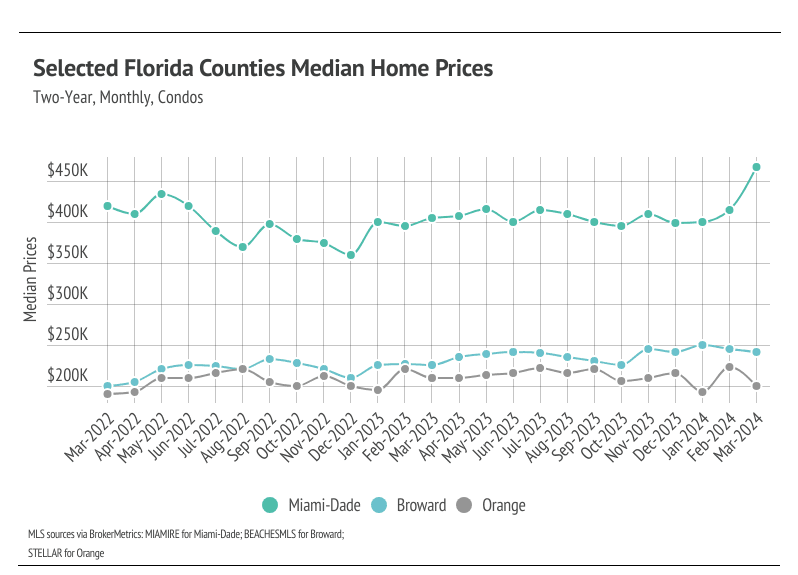

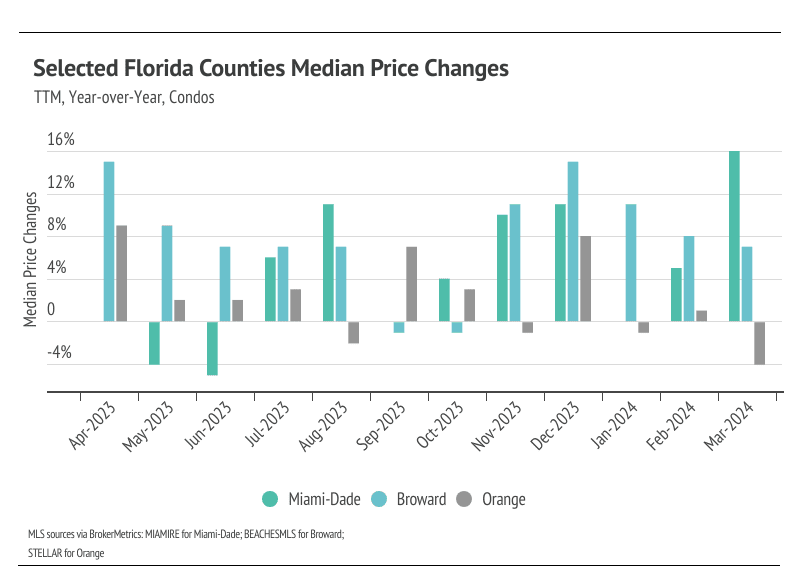

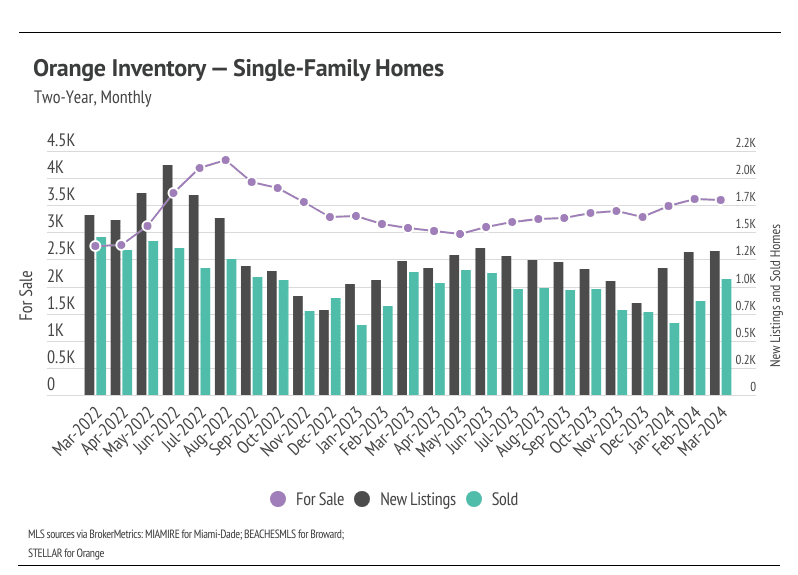

Miami-Dade single-family home and condo prices rose month over month, reaching new all-time highs. We expect prices in Broward and Orange to hit new highs in Q2 2024.

-

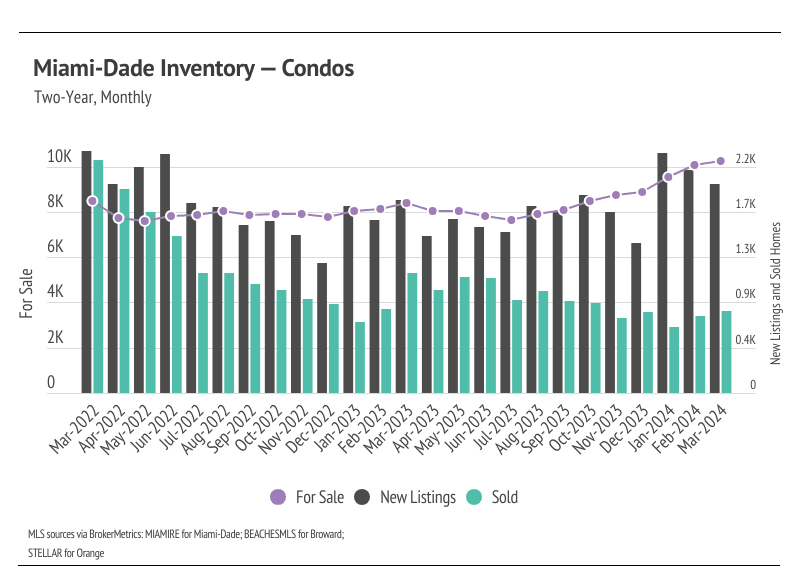

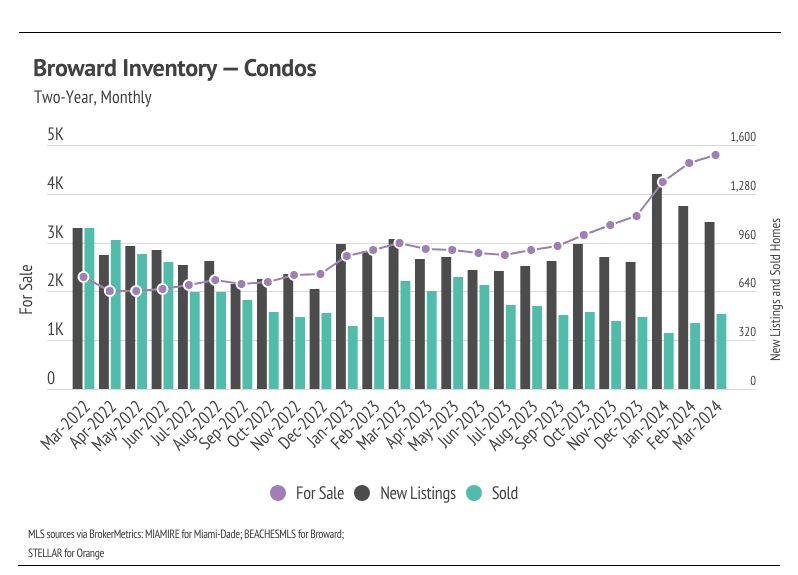

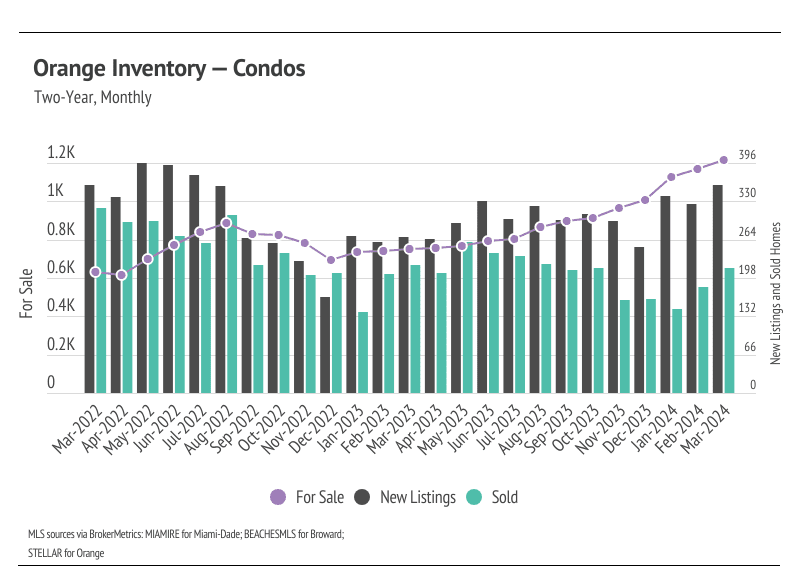

Active listings fell for single-family homes month over month but hit new two-year highs for condos. The market is also seeing more new listings and increasing sales, which are both good for a healthier market.

-

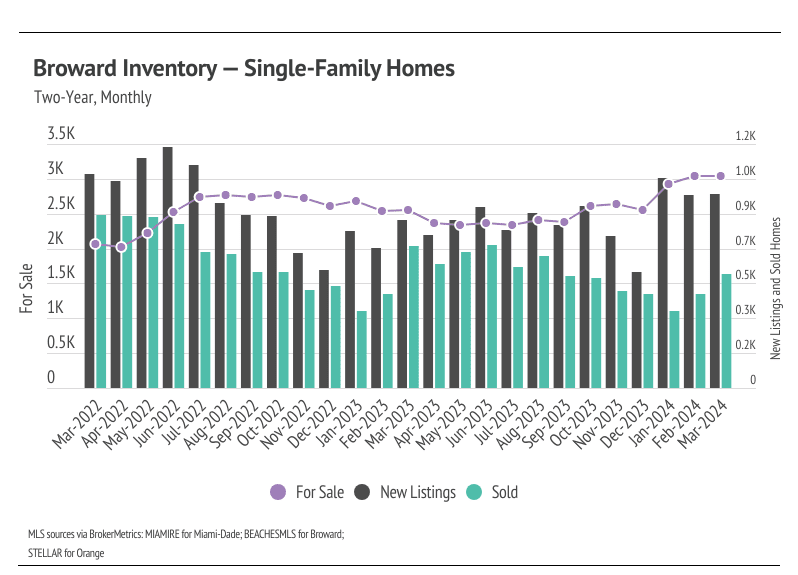

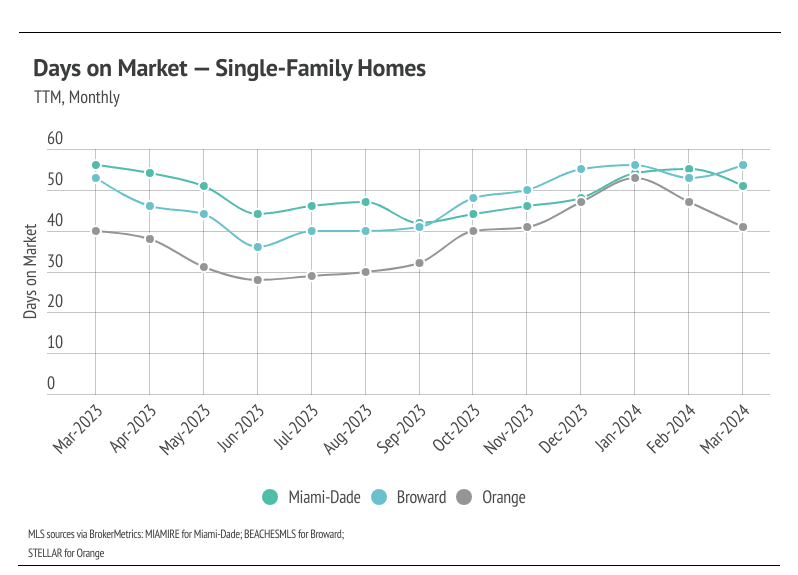

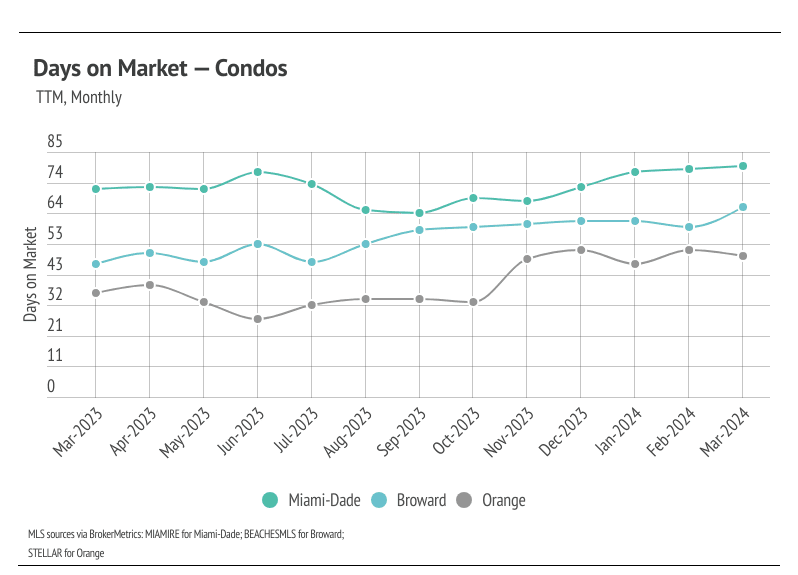

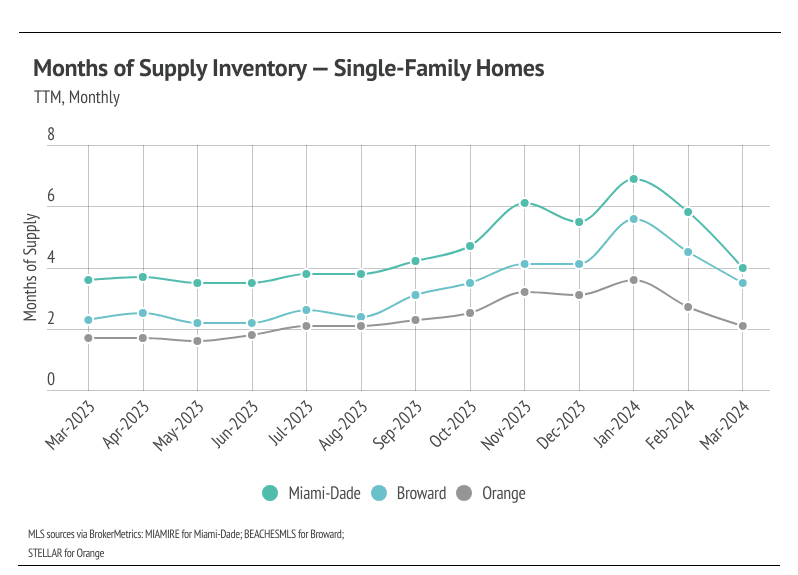

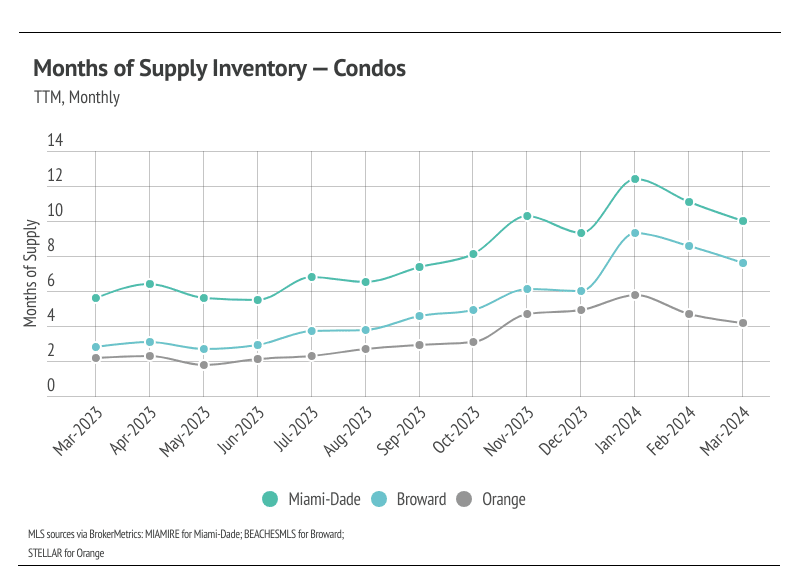

Months of Supply Inventory fell across markets over the past two months. Currently, for single-family homes, MSI indicates a sellers’ market in Orange and Broward and a balanced market in Miami-Dade. For condos, MSI indicates a balanced market in Orange and a buyers’ market in Miami-Dade and Broward.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

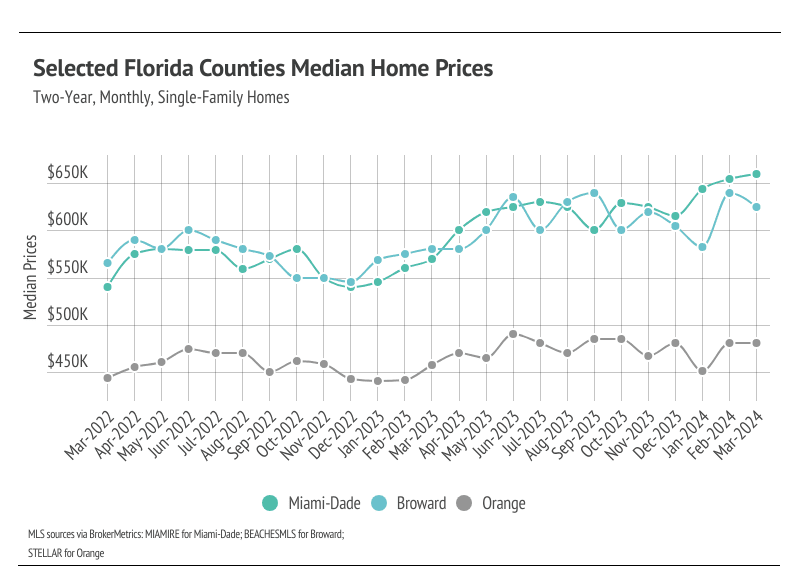

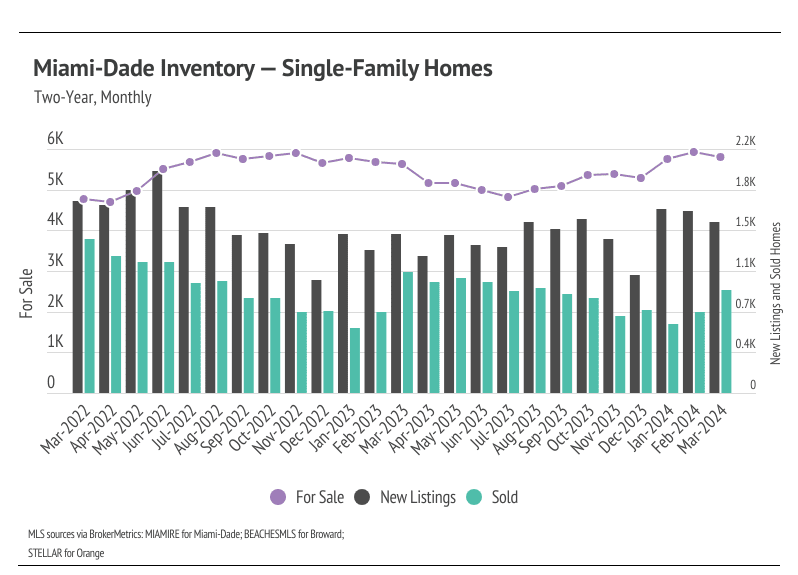

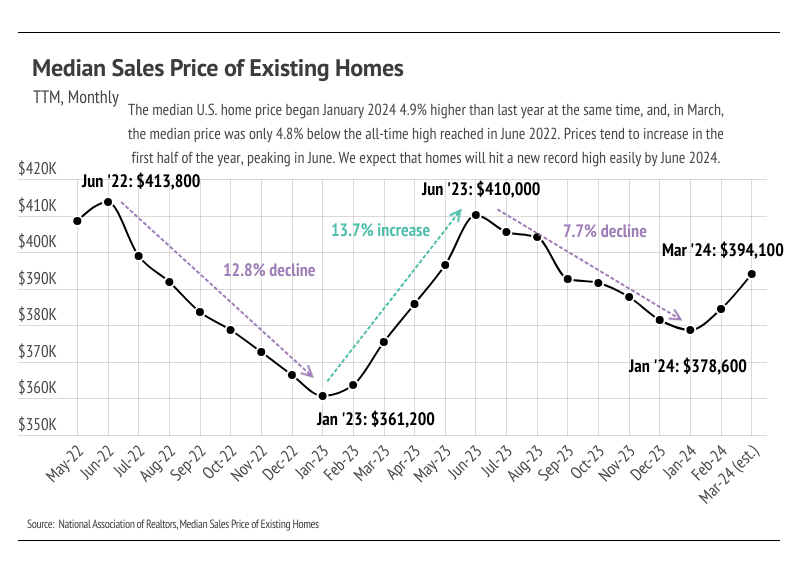

Median single-family home and condo prices in Miami-Dade hit all-time highs in March

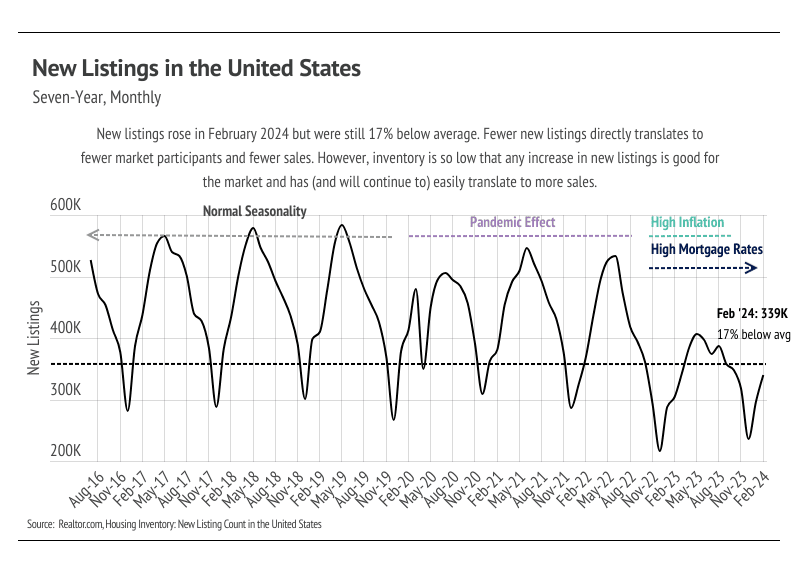

In Florida, home prices haven’t been largely affected by rising mortgage rates — even recently reaching all-time highs during a period of rapidly rising mortgage rates. In February, the median single-family home prices in Miami-Dade and Broward, and the median condo price in Orange, all hit all-time highs. In March, Miami-Dade single-family home and condo prices continued that trend, reaching new all-time highs again. Prices almost never peak in the winter months, indicating that home prices will likely rise to a new high in almost every month during the first half of the year. Florida has been in an interesting spot recently, where residents are starting to move because home insurance prices have risen, which has brought more listings to the market. However, demand is still strong, so the low but rising inventory and new listings will only raise prices as demand grows. More homes must come to the market in the spring and summer to get anything close to a healthy market, and we are already seeing more new listings coming online.

High mortgage rates soften both supply and demand, but at this point rates have been above 6% for 16 months, and rate cuts will likely occur sometime this year. Potential buyers have had longer to save for a down payment and will have the opportunity to refinance in the next 12-24 months, which makes current rates less of a limiting factor. However, high demand can only do so much for the market if there isn’t supply to meet it.

Inventory declined for single-family homes in March, but reached a two-year high for condos

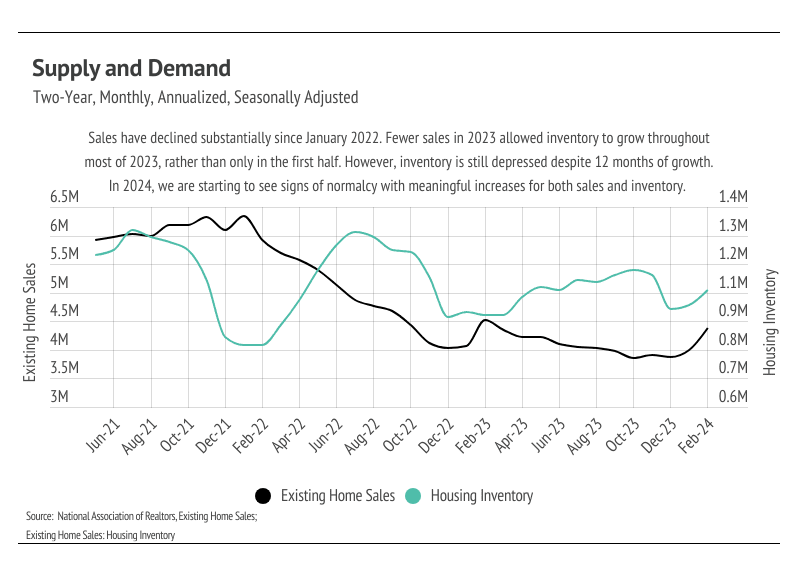

Florida inventory patterns have been atypical since the pandemic started. Homebuyers flocked to Florida, dropping inventory to hyper-low levels. Only recently has inventory begun to build. Low inventory and new listings, coupled with high mortgage rates, led to a substantial drop in sales and a generally slower housing market from June 2022 to the present. Typically, inventory begins to increase in January or February, peaking in July or August before declining once again from the summer months to the winter. In 2023, inventory patterns didn’t resemble the typical seasonal inventory wave. Luckily, inventory has grown substantially — especially for condos. The number of new listings coming to market is a significant predictor of sales, and the increase in new listings over the past few months has led to an increase in sales. Demand is definitely ramping up in Florida, and the next three months will be critical to our understanding of the market. More supply will mean a healthier market.

Months of Supply Inventory fell in February and March 2024, indicating the market is getting more competitive for buyers

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around four to five months in Florida, which indicates a balanced market. An MSI lower than four indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while an MSI higher than five indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI rose significantly in the second half of 2023, largely due to the decline in sales and longer time on the market, and continued to rise in January 2024. However, January is unusual in that new listings jumped higher across the selected areas, which caused inventory to rise rapidly month over month and increased the proportion of active listings to sales. As expected, in February and March, MSI corrected and declined significantly across markets. Currently, for single-family homes, MSI indicates a sellers’ market in Orange and Broward and a balanced market in Miami-Dade. For condos, MSI indicates a balanced market in Orange and a buyers’ market in Miami-Dade and Broward.

We can also use percent of list price received as another indicator for supply and demand. Typically, in a calendar year, sellers receive the lowest percentage of list price during the winter months, when demand is lowest. Winter months tend to have the lowest average sale price (SP) to list price (LP), and the summer months tend to have the highest SP/LP. In Q1 2024, SP/LP was slightly higher than last year, meaning we expect sellers overall to receive a higher percentage of the list price throughout all of 2024 than they did in 2023.